Explainer: Governmental vs. Proprietary Funds

The City of Elkins sometimes hears questions from the public along the following lines:

- Why are you raising sewer or water rates when the city just started receiving approximately $1 million in sales tax revenues?

- Why are you raising sewer rates when there is money left over after construction of the new water plant?

- Why did the police department get new vehicles when the water system was getting short on funds?

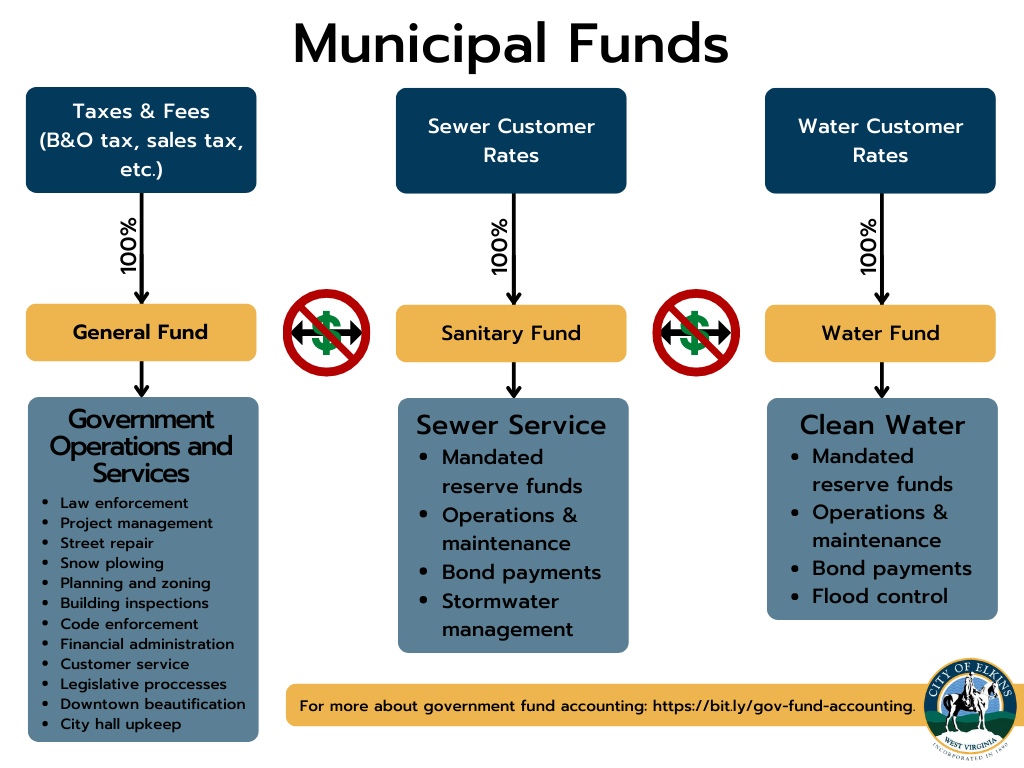

The simple answer to questions like these is that it is illegal to transfer money between the city’s General Fund and any of our three enterprise funds such as the Sewer Fund, Water Fund, and Sanitation Fund.

Learn more about governmental fund accounting and enterprise funds, some of the ways government accounting methods differ from the accounting methods used by private businesses, and the significant restrictions imposed by state law concerning how the City of Elkins can spend various categories of revenues.

Fund Accounting

Although governments and private businesses have much in common, one crucial difference has to do with their accounting methods—that is, how they organize and account for resources, revenues, and expenditures. This is because private businesses are organized with a focus on profitability, while governments are organized with a focus on public accountability.

As a result, private businesses do not necessarily face legal restrictions restricting how they can spend certain categories of revenue—but cities do. Cities and other governments are restricted in how they can spend revenues; what the restrictions are depends on the sources of the revenues. These restrictions are reflected in the accounting system governments use, which is called fund accounting. Fund accounting is a method of recording financial resources and activities within restricted categories.

Types of Funds

For local governments, the three main types of fund are governmental, proprietary, and fiduciary.

- Governmental funds account for the core services and activities of a city government. Governmental funds—and the activities they pay for—are mostly tax supported.

- Proprietary funds account for business-like activities of the government, such as utilities. Proprietary funds are concerned with activities financed by self-generated revenues.

- Fiduciary funds hold resources in trust for entities or individuals other than the government, such as employee pension funds. (not discussed here)

Governmental Funds

As mentioned above, governmental funds account for the core services and operations of a city government. A city’s primary governmental fund is called the General Fund. The General Fund is the city’s basic operating fund. One way of thinking about a General Fund is that it accounts for all monies not required by law to be accounted for in proprietary funds.

The revenue sources for the Elkins General Fund are taxes and fees. There are more than two dozen categories of revenue that flow into our General Fund. The four largest are property taxes, business taxes, hotel taxes, and sales tax. For the fiscal year ending June 30, 2020, the City of Elkins budgeted for about $5.5 million in General Fund revenues.

In Elkins, as in most cities, the General Fund pays for activities like street repairs, snow plowing, the police department, planning and zoning, building inspections, code enforcement, financial administration, customer service, legislative processes, downtown beautification, the functioning and upkeep of city hall, and many other basic services and operations of the city government.

Proprietary Funds

Also as mentioned above, proprietary funds account for business-like activities of the government. The most common example is utilities. Under West Virginia law, sewer, water, and other utilities operated by a municipality must be run as standalone businesses, with their resources, revenues and expenditures accounted for in a type of self-balancing proprietary fund called an enterprise fund. Here in Elkins, our enterprise funds are the Water Fund, the Sewer Fund, and the Sanitation Fund.

One of the defining characteristics of an enterprise fund is that no money can be transferred in or out of it. The only allowed income for a utility enterprise fund is the money that the utility’s customers pay for service (also known as “the rates”). The only allowed use of that income is for the operation, maintenance, and development of that utility.

Why These Restrictions Exist

The purpose behind the restrictions described above, again, is accountability. If money paid by, say, the sewer utility’s customers could be transferred from the Sewer Fund into the General Fund, or vice-versa, unscrupulous officials might be tempted to do so to cover deficits and avoid unpopular policy changes.

By concealing the true costs of basic government services (accounted for in the General Fund) or utility operations (accounted for in the Sewer, Water, or Sanitation Funds), allowing the free flow of monies between funds could reduce public accountability. Lack of restrictions on inter-fund transfers could conceal poor budgeting, ineffective planning, and other mismanagement that could spell disaster for the city and/or its utilities in the long term.

So the Next Time Someone Asks

- Why can’t tax proceeds be used for water or sewer projects?

- Why are you raising sewer (or water) rates when the city just started receiving approximately $1 million in sales tax revenues?

- Why are you raising sewer rates when there is money left over after construction of the new water plant?

The answers to these kinds of questions stem from the requirement that general, sewer, and water revenues and expenditures be accounted for separately.

Because of this requirement, it would be illegal to use sales tax (or any other General Fund) revenues to pay for sewer, water, or sanitation expenses. And it would likewise be illegal to use monies generated from one utility’s customers to pay for the projects of another utility.

That isn’t always the answer city residents and business owners want to hear. But it’s the only one we can give if we are to remain committed to financial transparency and compliance with all applicable financial laws, rules, and regulations.